Awareness for a pure term plan is growing now a days . You might have heard about term plan insurance before & if you are planning to buy it, CONGRATULATIONS!! You have made a right choice.

I have found many people arguing that buying a term plan is just a waste of money, as they do not receive any guaranteed benefit in return on the maturity of policy term and even agents don’t encourage to buy a term plan.

Why is it so? Are endowments plans better than term plans?

Of course NOT!!

Before coming to the conclusion, Let us understand the meaning of term plan and endowment plan.

What is Term Plan?

What is Term Plan?

Term Plan is a pure insurance cover which means it covers only death risk. So, if insured person dies during the policy term period, the entire Sum Assured amount would be paid to the Nominee. Thus, no survival or maturity benefit is provided.

It gives ultimate benefit of huge insurance cover with low premiums. Thus, it fulfills the purpose of Pure Life Insurance.

What is Endowment Plan?

Endowment Plan is the combination of both insurance & investment as it covers both Maturity benefit as well as death benefit.

In simple words, if insured person dies during the policy term, nominee gets the Sum Assured as the Death Benefit. And, If the policy holder survives until the end of the policy term he would receive maturity benefit. i.e: Maturity Benefit: Sum Assured + Accrued Bonuses.

Incase of Endowment Plans, The Premiums are highly expensive and Sum Assured benefits doesn’t even fulfill the required Insurance need of the person.

Now, Let’s analyze with the help of example that how a term plan is a better option if we combine it with some other investment options like Mutual Funds – which works just as a investment avenue.

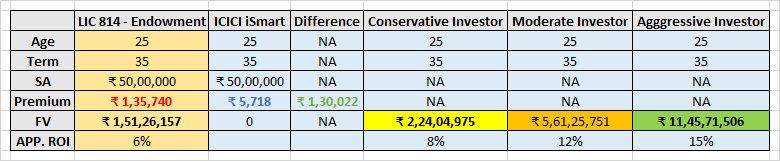

Let’s take a look at the comparison between an Endowment Policy & a Term Plan for a 25 Years Old.

Comparison of Endowment Plan with Term Plan + Mutual Funds

Now, let me show you a brief calculations to help you understand better about Term Insurance & Endowment Plans.

In the above table I have made a brief comparison between LIC – New Endowment Plan (Table 814) & ICICI IProtect Smart (Term Plan) which explains the Return on Investment’s if done separately can outperform the Endowment Plan Performance.

In the LIC New Endowment Plan if you are 25 Years Old and Take a 35 Years Policy Term with 50 Lakhs Sum Assured then you need to Pay an Yearly Premium of Rs. 1,35,740/-

So as you can see, a Term Plan for 25 Years Old with 35 Years Term and Sum Assured of Rs. 50 Lakhs costs just Rs. 5718/- per annum of ICICI Prudential IProtect Smart.

So, difference of the paid premium in LIC Endowment Plan and ICICI I Protect Smart is Rs.1,30,022 per annum. If Invested in Mutual Funds for Conservative Investors, Moderate & Aggressive Investors – all three outperforms the Returns you get from LIC Endowment Plans.

As you can see in the Table above that even a Conservative Investor makes better returns than Endowment Plan with a whopping difference of around Rs. 73 Lakhs. Whereas, an Aggressive Investor makes almost Rs. 10 crores more than an Endowment Plan with a similar risk cover of Rs. 50 lakhs at a cost of just Rs. 5718/- per annum which is to be paid to his/her nominee incase of any unforeseen event occurs.

The premiums of Term Plan is the lowest among all other insurance policies because there is no investment component & thus makes it possible for everyone to fulfill their purpose.

Disclaimer: All above calculations and explanations are just for educational purpose. No Advice or Endorsement has been made for above companies in any form. Kindly consult Financial Advisor before taking any financial decisions.

Now, before concluding let me take you through the main points which you must remember before taking any decision.

Points To Remember

-

TREAT INSURANCE AS INSURANCE

I have seen most of the people who buy a life insurance policy either for the sake of Tax Saving or for investment purpose. If you are one of them, let me tell you, Insurance does not mean Tax Saving or Investment, it simply means to give a financial protection to your family when you are not around as they do not loose your financial support even if they loose you.

The Greatest Myth is that Insurance is an Investment Product: Most of the people buy Life Insurance Policies because they think they are investing money to fulfill their financial goals but let me clear you, if you are doing so then you’re doing WRONG! As Such Insurance Policies like Endowment Plans will give Average Return on your Investments barely 6%.

Insurance in its purest form is an expense not an investment & it must be treated like an expense rather than investment to cover any unforeseen incident. Buying an endowment plan will neither serve your objective of investment nor insurance.

-

INSURANCE PLANS ARE MOSTLY UNDER INSURED

Let us assume you are 30 years old & your annual income is 20 Lakhs, Would Rs.5-10 Lakhs Insurance cover be sufficient for you?

Almost everyone has an insurance cover BUT the major problem is that they are mostly under insured.

Do not take such small insurance cover as Indians are already highly under insured.

Insurance helps you to solve bigger risks as it’s a process to transfer your financial risk to an insurance company which further take care of financial responsibilities of your family when you are not around, consider the following points before you take an insurance cover:

It must cover

- Living Expenses of Spouse and Dependents.

- Future Financial Goals like Children’s Higher Education and Marriage Expenses.

- Your Unpaid Loans and Other Liabilities.

Most people are under insured because they bought policies like Traditional Plans which are very costly and don’t even fulfill adequate insurance needs.

-

TERM PLAN IS A MUST BUY IF YOU HAVE DEPENDENTS

When you are young & single, you might not have anyone financially dependent on you.

After marriage, your responsibilities also increases with your spouse and children so one must insure the financial well being of their family.

Term Insurance is a pure risk cover and a product which is an absolute must for every individual who have dependents relying on their income.

-

START EARLY AS YOU CAN

Do not delay your decision to take term insurance life cover as the reason is very simple. Your premium is likely to increase with your age, which means you need to shell out more money from your pocket every year if you delay insuring financial needs of your family.

Let me show you how premium hikes with the age through below table:

| Current Age | Policy Term (Till 60) | Annual Premium |

| 25 | 35 | 9332 |

| 30 | 30 | 10907 |

| 35 | 25 | 13348 |

| 40 | 20 | 17078 |

RelatedPosts

So, do not delay decision as you can lock the premium amount today and enjoy the benefits of same premiums till the remaining tenure of your policy.

3 KEY BENEFITS OF TERM INSURANCE

- Affordable Premium’s

- Peace of Mind

- Comprehensive Financial Security

Conclusion

In the end, I would like to share few things with you that to make a Person’s Life Financially Stable one must have an adequate insurance cover – which only a Term Plan can fulfill. One must never take an insurance policy for the sake of investment.

One more thing which I would like to add, specially for the young mates is that – If you’re young and healthy it doesn’t mean you don’t need a life insurance cover. Life Insurance cover is a must for you if you have dependents on you and taking it when you’re young would be one of the best decisions of your life to make a financial stability when it comes to your family.

{kind=link}

Comments 1